Tax credits, qualified tuition programs, income exclusions and penalty waivers can help taxpayers with education expenses.

A tax credit will reduce your taxes dollar for dollar and may even be refundable. A qualified tuition program is a program in which you are able to contribute to and accumulate earnings tax-free if funds are used for education expenses. Income exclusion is a means of excluding income from gross income because the income is offset by qualified education expenses. The penalty waiver is the avoiding of the 10 percent penalty on early IRA withdrawals because you used the funds for higher education.

You are able to apply one or a combination of these benefits to your tax return that affords you the best possible tax outcome. Each benefit has its own set of qualifications, rules or limitations. One common restriction is that an expense can be used only once.

CREDITS

There are two education credits available: the American Opportunity Tax Credit and the Lifetime Learning Credit. These credits are based on the expenses you paid during the calendar year, even if for classes taking place the following spring. Example: If you pay in 2018 the 2019 spring semester bill, you can use these expenses to calculate the 2018 credits.

The American Opportunity Credit is a partially refundable credit. It credits up to $2,500 per student (100 percent of first $2,000 of expenses and 25 percent of next $2,000). Forty percent of this credit may be refundable. The student must be in his first four years of an undergraduate degree program and must be enrolled at least half-time.

The Lifetime Learning Credit is a nonrefundable credit. It credits up to $2,000 per return (20 percent of up to $10,000 of expenses). The student may be an undergraduate or a graduate candidate and enrolled in either a degree or a non-degree program. This credit is available for an unlimited number of years.

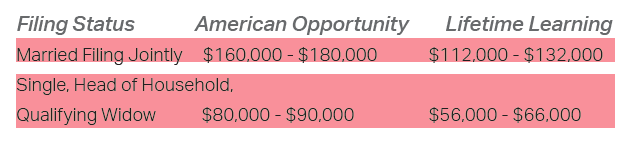

The credits are reduced or phased-out when the modified adjusted gross income reaches certain amounts (see chart). Married taxpayers filing separately do not qualify for these credits.

The qualified education expenses for both credits include tuition, fees, books and supplies and equipment. However, for the equipment to qualify for the American Opportunity Credit, it must be required for enrollment. For the equipment to qualify for the Lifetime Learning Credit, it must be paid to the eligible educational institution as a condition of enrollment. The qualified education expenses may be for the taxpayer, spouse or their dependent.

If you are eligible to claim both credits for the same candidate for the same year, you can choose to claim either credit, but not both. The candidate cannot be a convicted federal or state felon for possessing or distributing a controlled substance. And, the candidate must have a social security number or an individual tax identification number before the filing of the tax return. Parents can shift the credit to the dependent student by not claiming the student as a dependent on their tax return.

MODIFIED ADJUSTED GROSS INCOME PHASE-OUT

SAVINGS PLANS

Qualified tuition programs are of two types: prepaid programs and education savings accounts. These programs involve making non-deductible contributions for named beneficiaries in earlier years wherein earnings grow tax-free. In the years these funds are distributed to pay for qualified education expenses, the funds are tax-free. Earnings portion of distributions not used for qualified higher education expenses will be subject to a 10 percent penalty.

Qualified higher education expenses include:

- Tuition, fees, books, supplies and equipment required for attending an eligible school.

- Room and board if the student is enrolled at least half-time.

- Expenses for special needs services incurred in connection with enrollment.

- Cost of computer and related equipment, certain software and internet access.

The ESA can be used to pay qualified elementary and secondary expenses (K-12th grade):

- Tuition, fees, academic tutoring, books, supplies and other equipment needed for enrollment at a public, private or religious school.

- Special-needs services for a special–needs beneficiary.

- Room and board, uniforms, transportation and supplementary items and services (e.g. extended day programs).

- Cost of computer technology or equipment or internet access and related services.

Except for special needs beneficiaries, any balance remaining in the ESA not used for education expenses must be distributed within 30 days after the beneficiary reaches 30 years of age. Any distributions from a prepaid program not used for higher education are subject to a 10 percent penalty. There is a phase-out when modified adjusted gross income reaches certain amounts.

INCOME EXCLUSIONS

Qualified scholarship and fellowship amounts are excluded from gross income if received by a degree candidate and used for tuition, fees, books, supplies and equipment required by the education institution. Amounts received by a non-degree candidate are taxable.

Interest earned on Series EE bonds (issued after December 31, 1989) or Series I bonds is excluded from income for qualified taxpayers if the bonds are used for qualified educational expenses. Qualified educational expenses are tuition and fees for the bond owner or his spouse or dependent at a qualified educational institution (e.g. college, university or vocational school). Room, board and books do not qualify. This exclusion is not available to married taxpayers filing separately.

PENALTY WAIVER

The 10 percent early withdrawal penalty is waived on IRA withdrawals if the funds are to pay qualifying education expenses. Qualified education expenses include tuition and fees, books, supplies and equipment required for enrollment as well as room and board. The student (e.g. taxpayer, spouse, child or grandchild) must be enrolled at least half-time as an undergraduate or graduate candidate.

These education tax incentives can be difficult to comprehend. Get the institution’s 1098-T and QTP’s Form 1099-Q after year-end and see your tax professional for help.

Perkins is a CPA at Tina Perkins, CPA, P.A., 4048 Popps Ferry Road, D’Iberville, MS 39540. Reach her at (228) 392-2991.